Universal Music Group

Dreams & Reality

Universal Music Group is down 45% in 9 months, trading 14% below its 2021 IPO despite growing revenue and EPS >50% since. Recent selling comes from the scrapped pursuit of a US listing, and the Iran war pressuring European equities; but the yearlong drive lower has been a structural rerating. UMG was a sexy secular compounder at the chokepoint of the music industry’s streaming evolution. Now streaming appears saturated in developed markets, AI threatens to dilute the royalty pool, and UMG looks like a mature, soggy MSD grower at best, with a weaker than expected position in the value chain.

Given the depth and reliance on UMG’s catalog, investors expected more aggressive terms with Digital Streaming Providers (DSPs) like Spotify, but DSPs have captured more of the spoils from price hikes. At the same time, some of UMG’s top artists have negotiated better deals and commanded equity ownership of their catalogs. In turn, growth decelerated, margins contracted, estimates were revised lower and the stock has languished. Meanwhile, CEO, Lucian Grainge pocketed ~$400M in compensation, a package so egregious it’s outmatched only by David Zaslav.

The music has stopped for Quality-compounder-bros, but I’m a salty Value guy who’s been waiting for this fade since Ackman was pumping his super SPAC with a sock puppet. My time has come.

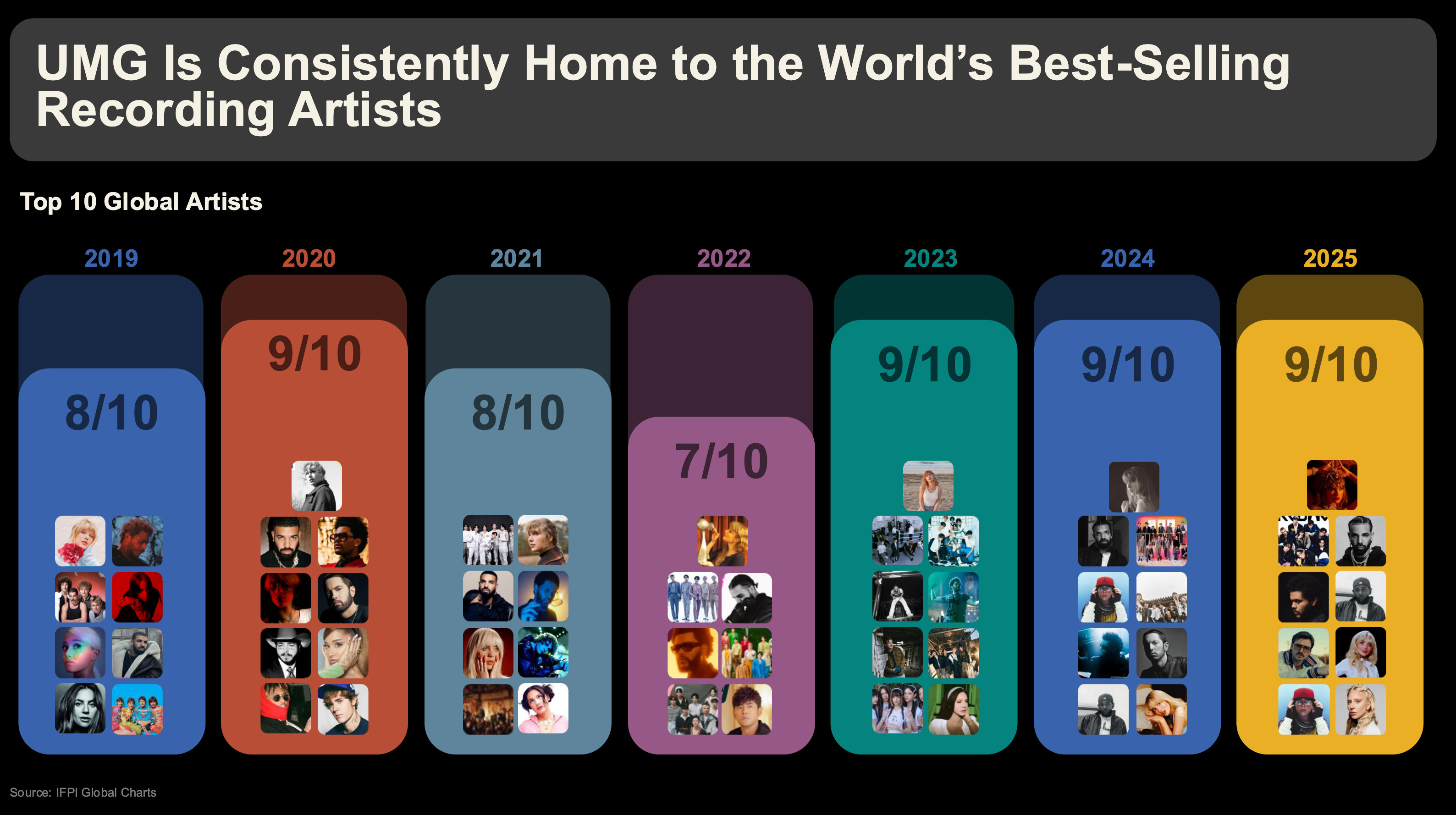

UMG owns an irreplaceable catalog, has the best artists, the largest scale and operates an oligopoly alongside Sony and Warner Music Group. The music industry transformed and consolidated in the 2000s after Napster blew up their model. The pirating era was a total apocalypse and catalogs of timeless artists like The Beatles and Bob Marley were bought at distressed values. They will never sell that cheaply again; hence no one can ever build another UMG. Today’s hottest stars may want more equity, but they can’t manage the infrastructure of global stardom and need the majors for distribution. Out of Billboard’s 2025 Year-End Hot 100 songs, 45 of the featured artists are signed to UMG. The moat is very wide.

At €15.50 UMG trades at

15x FY26 adj EPS, 18x GAAP

11x FY26 EV/EBITDA

14x FY26 EV/EBIT

5.5% FCF yield

3% dividend yield

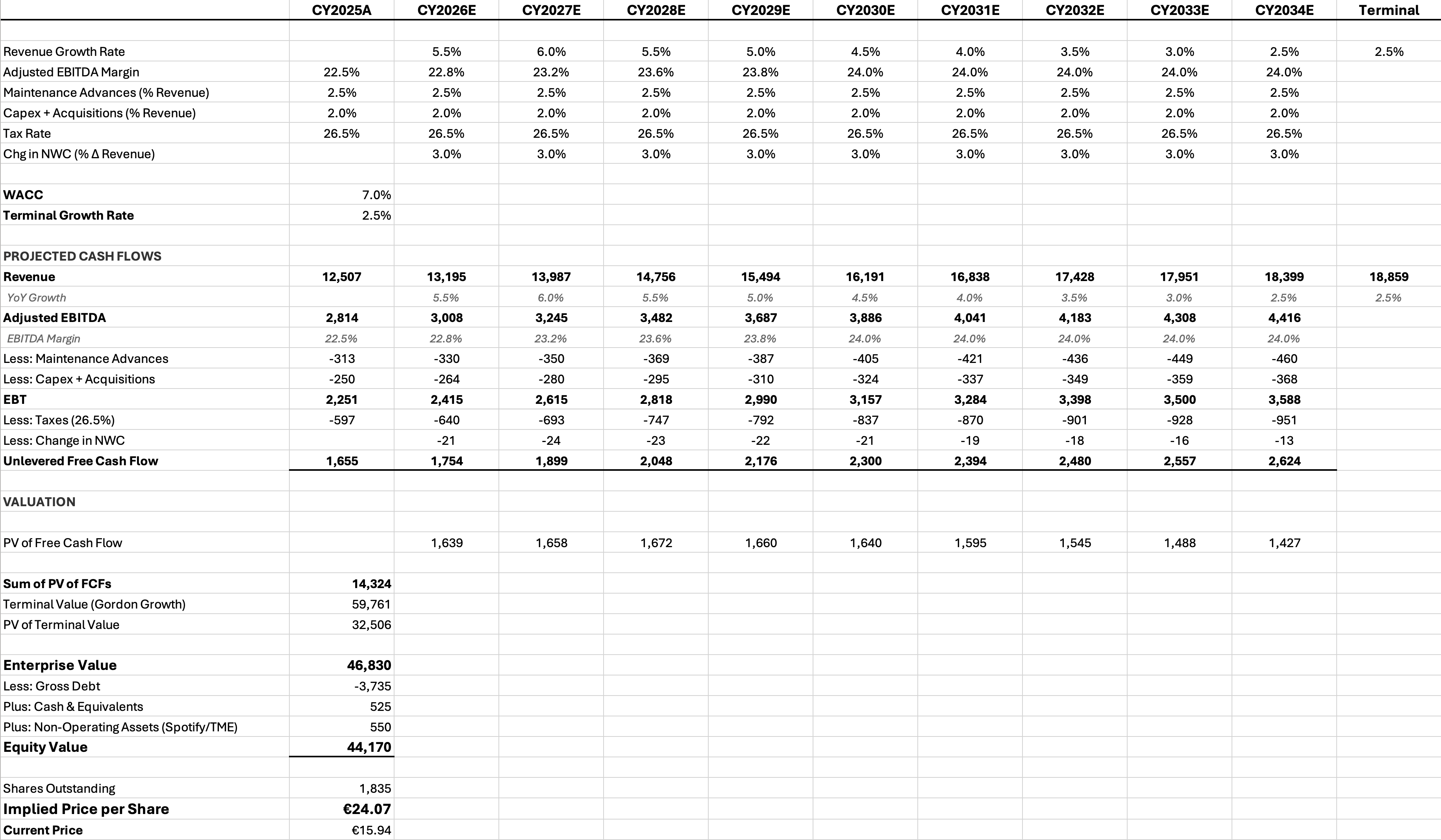

Much of UMG’s catalog depreciates on the balance sheet, but are appreciating assets in reality. The catalogs of The Beatles, Elton John, Louis Armstrong, are more valuable today than when UMG acquired them. This makes UMG one of those rare cases where EBITDA is not entirely a euphemism for “bullshit earnings.” Paying out advances to new artists is a real ongoing expense, but amortization on the catalog should be added back, Something like EBITDA minus maintenance advances is closer to UMG’s true earnings. The replacement value of UMG’s catalog dwarfs the book value. This inflates P/B, and makes UMG screen worse on P/E because the E is artificially depressed by catalog amortization.

A conservative DCF grounded by EBIT and FCFF, modeling MSD growth says UMG at ~€16 is fair value. But using EBITDA minus maintenance advances gets me to €24 per share. 55% upside. Sell side focuses on EBITDA which is even easier for UMG to grow. UMG simply buys more catalogs and pays out advances to more artists resulting in more D&A. I see further upside to estimates from ARPU expansion driven by Streaming 2.0 and AI licensing agreements. This is an embedded option for an incremental high margin revenue stream. UMG also owns a stake in Spotify worth ~$3B marked to market.

The narrative surrounding UMG is reaching a fever pitch of pessimism. This is a high-quality set of assets with a wide and durable moat, and predictable growth. While near-term catalysts may be limited, I view €15.50 as an attractive entry point with a substantial margin of safety.

The Bear Case

Bear Case 1. Deceleration. Streaming matured faster than expected.

Bear Case 2. AI slopapalooza will dilute the royalty pool.

Bear Case 3. Artists want equity in their masters and are signing shorter deals resulting in worse economics for UMG.

Streaming Saturation

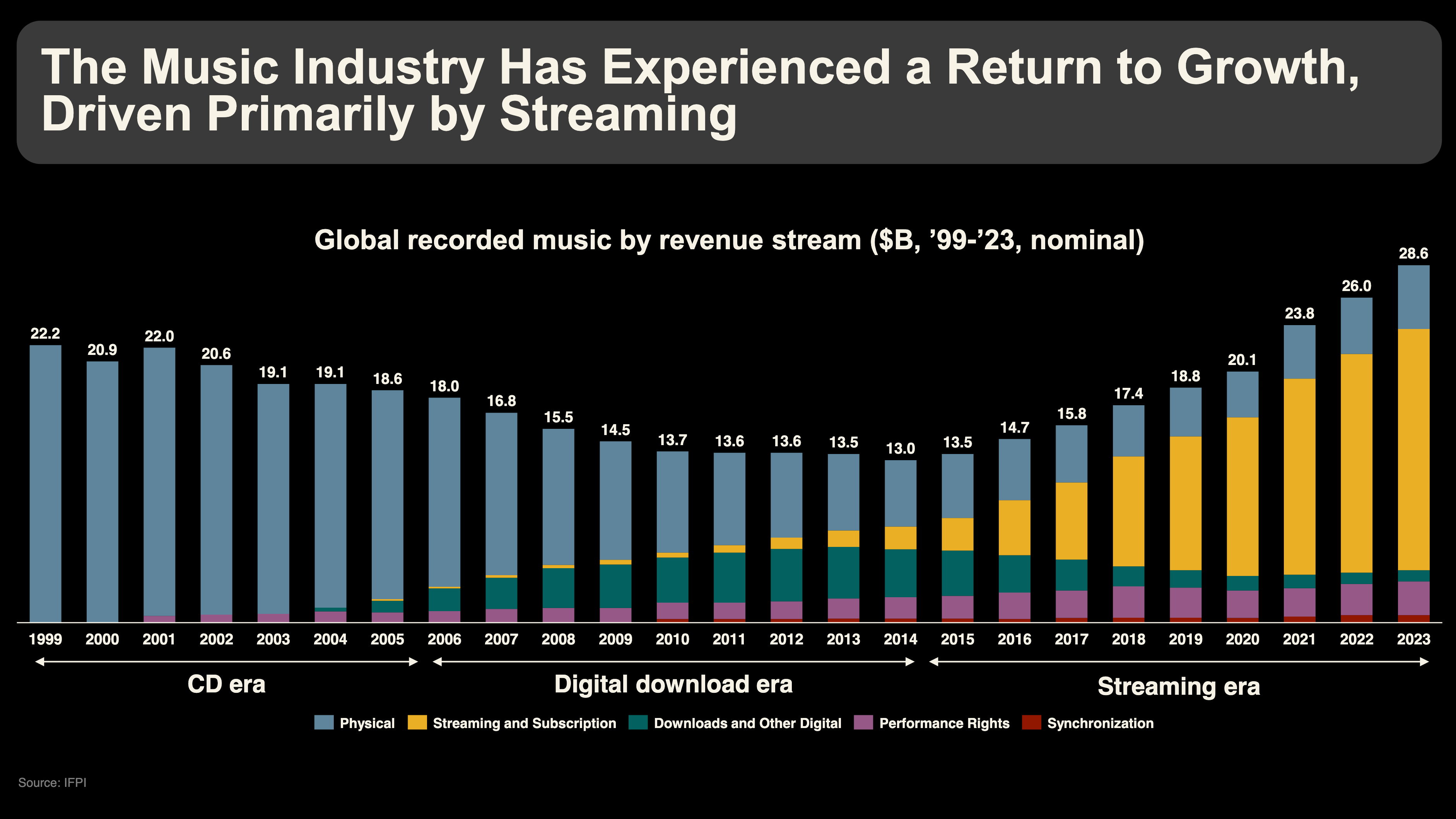

Driven by streaming, global recorded music revenue more than doubled from $15B in 2015 to $32B in 2025. But developed markets appear to be plateauing at 40-50% penetration, and even if emerging markets grow >15% annually, if DMs are only growing 1-3% the blended ARPU per incremental sub is declining. Not great, Bob. Any future growth in DMs is entirely a pricing story. Or is it?

>90% of Gen Z streams music, whereas most Boomers are unlikely to have a Spotify subscription. Penetration will naturally grow with aging populations and DSPs are still an incredible value. A single CD in the 1990s cost $25 in today’s dollars. Apple Music gives you unlimited access to every album in history (just about) for $10.99 per month. In 2023, Spotify took price for the first time in over a decade. Individual and family plans are up >30% with minimal churn, in line with Netflix. There’s still room for ARPU expansion and UMG captures a direct share of every price increase. UMG has plenty of runway for growth, just not the mid-teens growth that justified premium multiples.

Streaming 2.0

The most obvious sign DM sub growth is unlikely to reaccelerate is hype around Superfan tiers. For $17-20 per month hardcore fans get higher fidelity streaming, pre-sale concert access, and exclusive content. Supposedly. Superfan tiers have been teased for years, but there’s still no clear roll out date. It’s also unclear what any Live Nation agreement for pre-sale tickets would look like, but it won’t be cheap. Tencent Music’s Super VIP tier has 20M subs paying 5x normal rates. That’s ~16% penetration. If 16% of Spotify’s ~290M subs sign up that’s 46M potential upgrades.

AI Dilution

If anyone can make generic background music with text prompts, they can upload it to CD Baby in 30 minutes and have it streaming the next day. Suddenly, everyone is a creator churning out endless amounts of slop, and the denominator of the royalty pool is greatly outpacing the numerator. Okay, but it’s already very easy to make music. Ask the Gorillaz. AI is just another instrument for creators. Talented vocalists who don’t have a band or producer may no longer need one. The daunting and complex audio engineering software needed for mixing and mastering may soon become easy enough for a child to operate. AI could be a growth lever for UMG that enables their talent to produce more content at a faster pace with lower costs.

AI looks like the MIDI (Musical Instrument Digital Interface) revolution of the 1980s, a breakthrough that allowed electronic instruments from different manufacturers to talk to each other. Overnight, a basement producer with a keyboard, sequencer, and a drum machine could arrange tracks and make complete songs without session musicians or a full studio. This is why all the 1980s music sounds like it was made on a cheap, synthy keyboard. It was. MIDI paved the way for new genres like Hip-Hop and Techno. It made music production exponentially cheaper and grew the total pool of content, which was good for labels. Lower production costs, higher margins per release. Labels could sign more acts with less capital at risk. Pop production became formulaic, and a single producer could grind out hits with new artists who had no leverage to negotiate favorable terms.

UMG’s Streaming 2.0 deals with DSPs include provisions to explicitly prevent AI slop from diluting the pool. DSPs are inherently incentivized to remove low quality bot-driven streams so their platforms don’t become flooded with garbage. AI generated background music competes with stock music that was already commoditized. This is not a real risk.

Recently, a poet using Suno created the AI persona Xanai Monet, and became the first “AI artist” to reach the Billboard charts. While this makes a fun segment for morning talk shows, I’m skeptical digital entities will ever be serious competition for stars like Rihanna and Taylor Swift. Live tours are crucial to building and maintaining a fan base.

AI Licensing - Embedded option

Partners

Udio - Settled copyright lawsuit. Licensed AI music platform launching 2026.

KLAY - All three majors have signed licensing deals.

Stability AI - Partnership for professional-grade AI tools for artists/producers.

Splice, BandLab, Soundlabs - Various AI tool development partnerships.

NVIDIA - R&D partnership for Music Flamingo discovery model, artist incubator, creation tools,

Active Litigation

Anthropic - UMG suing for $3B

Suno - UMG will likely reach a compensatory settlement, licensing agreement, and possible equity stake in Suno. WMG and Sony have settled separately.

UMG has licensing relationships with Google through YouTube Music that will probably fold in Gemini rather than a new standalone deal. Gemini, Anthropic and OpenAI license is likely a matter of when, not if. While the long term economics are opaque as of today, the AI narrative around UMG has been decisively negative, but I view it as either net neutral or positive.

Artist Equity

If artists own their masters, UMG becomes a licensee earning lower gross margins on its most valuable content. Top-tier artists are the only ones that have this negotiating leverage, but they matter most because they command the bulk of the streams. I view this as the strongest bear case.

The vast majority of UMG’s catalog, millions of recordings, is owned in perpetuity. No one is coming to renegotiate the Beatles’ masters, but under the 1976 Copyright Act, artists can reclaim copyrights after 35 years which is a low-profile risk to UMG’s middle-aged catalogs. The caveat is if sound recordings are classified as works “made for hire,” termination rights don’t apply. This has of course been UMG’s position in recent litigation, but labels can’t risk setting a precedent, which means UMG is likely renegotiating terms with artists who file termination notices. By 2030, everything from the late 70s-1995 becomes eligible. The late 80s and early 90s catalog is hugely valuable and coming into play. Nevermind by Nirvana becomes eligible this September. Depending on the new deals, this could squeeze margins over the longer-term.

There are maybe 20 artists in the world who can command a Taylor Swift or Kendrick Lamar-type deal. Labels owning the masters is still the norm and this won’t change for next gen mid-tier artists. 99.9% of emerging stars need upfront capital and would sell their soul for UMG’s distribution and marketing. Young artists aren’t thinking about their royalty split 20 years out, most of them just want to make music and get famous. It’s also telling that Taylor Swift, Kendrick, The Weeknd all have more than enough resources to operate as independents, yet they all chose to sign with UMG. That’s because UMG’s global infrastructure generates more total revenue for their music than they could generate alone. It’s a mutually beneficial relationship.

Macklemore - A Case Study

Macklemore is one of the most successful indie artists of all time. Thrift Shop was the first independently released song to hit #1 on the Billboard Hot 100 in 11 years. Macklemore LLC owned the masters and publishing but still relied on Warner Music Group’s distribution and would not have achieved such commercial success without it. Macklemore and Ryan Lewis earned a 50% take on digital sales whereas a standard deal would’ve been ~15-20% after recoupment. The Heist won four Grammys, had four singles on the Billboard Hot 100, Thrift Shop hit more than a billion views on YouTube, and Macklemore became a global superstar while capturing a much larger piece of the unit economics. It looked like a new era for independents had arrived.

“I’ve always wanted to own my music. I don’t want to give it away. I don’t want to be a puppet. No dollar amount to me is worth that.”

Rejecting the soulless corporate labels was part of Macklemore’s brand. He was self-made with total creative control. But despite his incredible momentum, his second album flopped and his career trajectory flat-lined.

“Part of that was just rebellion against the industry… Whatever is the norm of what radio is, fuck it. Let’s make what we want to make.”

They did, and it sucked. A major label would have deployed a massive team to develop a cohesive second album strategy. Macklemore maximized per-unit economics on one album cycle but left enormous lifetime earnings on the table. He beat Drake, Kendrick Lamar, Kanye West, and Jay-Z for Best Rap Album at the Grammys and his career peaked that very night. If he was signed to UMG and the label’s machine cranked out another three or four commercially successful albums, Macklemore would have sustained relevance, and his net worth would be 5x higher today even at lower per-unit economics. The label’s ongoing investment in career development separates a one-hit-wonder from a franchise.

Downtown Music Acquisition

As the cost of production has dropped, independent music has grown to nearly 50% of global streaming. AI tools may accelerate this trend, and to participate in this growth UMG completed its acquisition of Downtown Music Holdings (CD Baby, FUGA, Songtrust) in February. Downtown serves millions of independents with distribution and publishing admin. UMG captures recurring platform fees on their streams at lower margins, but the business scales with the long tail of indie, and provides valuable data on millions of artists which can be used as a feeder system of talent for UMG’s A&R pipeline.

Oligopoly

The technology we use to consume music may be completely different in 20 years. Spotify may not exist, air pods may not exist, but Elton John, Nirvana, Amy Winehouse, Tupac, Bob Marley and the rest of UMG’s catalog will still be featured on whichever platform we’re using. Every year the catalog compounds and new hits from current artists become tomorrow’s catalog. UMG’s scale gives it the most A&R scouts, the most label imprints, and the broadest genre coverage. Global teams who understand regional markets, sync licensing, radio, retail, and brand partnerships better than anyone in the music business are invaluable to artists. The best emerging talent wants to be on UMG’s labels because that’s where the biggest hits are made by the stars they idolize. These catalogs are irreplaceable. There will never be another UMG.

Model

Catalysts

AI licensing agreement with Suno, OpenAI, Anthropic settlement

Official roll out of superfan tiers in Spotify

US listing - UMG cited “market conditions” but still intends to pursue US listing

Earnings growth

Risks

DSP churn

Trend towards artist equity

Catalog and advance inflation

AI dilution

Copyright reclamation settlements

Disclosure

I am long UMG.

This newsletter provides general ideas, not personalized investment counsel. All materials associated with this subscription and website, including articles, reports, and other features, are published for informational, educational and entertainment purposes exclusively. This content does not constitute investment advice, nor should it be interpreted as such. Any actions you take or decisions you make based on this content are entirely your own responsibility. Neither the author nor any affiliated parties will accept liability for any loss or damage, direct or consequential, arising from the use of the information provided.

This service does not issue trading signals, specific buy/sell recommendations, or any directive to trade. Nothing presented herein constitutes a solicitation or an offer to buy or sell any security. All sources are publicly available, but this information may contain errors. There is no guarantee, explicit or implied, that any ideas or securities discussed will replicate past performance.

The author may hold positions in the securities mentioned in these publications; these will be disclosed at the time of writing. There is no guarantee that the author will continue to hold these positions.

Very good summary. I wonder how the egregious compensation could be brought down to a normal level, or how to prevent that Grainge's successors ever get such a perverse contract.

What do you think about Compagnie L’Odet + Bollore which trades at a steep discount to their stake in UMG?