Orange Swan

The Impact of The Highly Probable

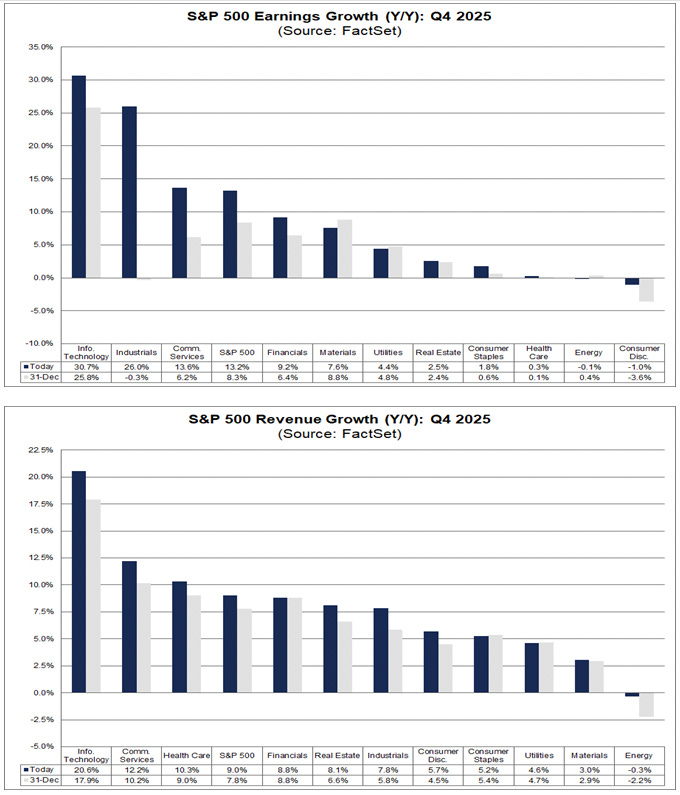

At 22x forward, the S&P is expensive compared to its own history, but with mid-teens EPS growth it’s a stretch to call it a bubble. If EPS grows 15% annually for the next 3 years and the price of the index remains unchanged it’s at 14.5x. You need a clear explanation for why downward revisions are coming if you want to call it a bubble, let alone call a top. There’s no recession coming in 2026 given the fiscal impulse: No tax on tips, no tax on overtime, $6,000 senior deduction, auto loan interest deduction, higher SALT cap, 100% bonus depreciation, full expensing of R&D, dozens of additional investment incentives alongside deregulation and a fed cutting cycle. Fuel to the fire in the first half. Whether it proves to be a sugar high remains to be seen, but Q425 EPS grew 13% and that was without the impact of the OBBBA.

Software’s bear market let some air out of a frothy sector, but this was not a major degrossing, money just moved into hardware and industrials. Shitcos getting crushed and a new crypto winter was a delightful second order effect. Or vice versa. They all peaked in October 2025, and the trashiest names are still up >100% from one year ago. Plenty of meat on the bone, but I don’t press high beta shorts down 30-50% in one month. I’ve learned that lesson the hard way and covered most of my shitcos over the past two weeks in anticipation of a vicious squeeze. If I don’t get an opportunity to reload at higher prices many will have 100% downside regardless. I view the frothiest sectors in the market taking a substantial beating as mildly bullish rather than a contagion risk.

Manifest Destiny

We all want a blow off top. Here’s how I think it happens: AI efficiency will expand margins and boost earnings with minimal labor market impact forcing analysts to revise S&P estimates higher. SCOTUS will likely rule against Trump tariffs within the next month reducing effective rates (unless they issue a stay). This is an off ramp for a deeply unpopular policy. While posturing about implementing tariffs through alternative policy avenues, I think Trump will pause China tariffs in April’s summit with Xi as a Hail Mary ahead of midterms. He loves the tariffs, he believes in the tariffs, but his only other option to avoid two years of impeachment trials and the risk of losing the senate is aggressive federal interference in local elections. TACO is the path of least resistance, but ¿por qué no los dos?

Without tariffs, the headlines around Trump’s economy would be disinflation and wage growth. With a backdrop of a booming AI supercycle, deregulation, fed cuts, modest job growth in the second half, and tariff relief, I expect market breadth to improve and take indices higher over the next 3-6 months. “But midterm election years are notoriously volatile and typically underpeform” you might say. True, but the sample size is small, and during the dot com bubble’s midterm election year (1998) the S&P rose 27% and Nasdaq was up 40%.

There are ~200-250 IPO planned for 2026, which feels paltry compared to >1,000 during the 2021 bubble. There’s a structural change here. First, private capital is abundant and going public often means lower marks. Second, all the garbage in private markets took advantage of the ZIRP-era-covid-bubble-SPAC-craze and already went public within the last five years. Major IPOs (rather than volume) may be the new sign of the top nearing. OpenAI, Anthropic, SpaceX all plan to IPO in 2026 and will soak up a lot of speculative dollars sloshing around in rolling bubbles. These mega IPOs sit at the center of the AI circle-jerk, but a true blow up has to coincide with a major deceleration in revenue growth and narrative hype around AI progress. If OpenAI and Anthropic gamma squeeze on debut then grind -80% lower as the market begins to doubt AGI and growth stagnates, the infrastructure will follow suit and a bear market will be unavoidable.

How The Bull Dies

We don’t need to reach the heights of the dot com bubble for a market top. Risk appetite is at extremes, founded in a Sci-Fi fantasy narrative (based on real tehcnological advances) and buoyed by intertwined leverage. Margin debt is not only at record nominal highs, the margin-to-free credit ratio is 6x, credit spreads are razor thin, and retail is all-in on equities. This bull is long in the tooth.

22x may not qualify as a bubble if the economy remains strong, but the primary driver of the economy is the AI build out and every CEO at the center of the AI bubble has acknowledged AI is a bubble! There’s an eventual doom loop likely to take shape: Doubts about progress will cause asset prices to decline. Asset prices declining will cause a recession. Recession will impact revenue growth in Mag 7 forcing hyperscalers to rein in capex and confirming fears that AI progress has plateaued without meaningful ROI. Diminishing returns on LLMs despite massive scale, leads to a tremendous compute and memory glut as the entire complex implodes.

Given the concentration, when hyperscalers roll over, down goes the index. Post Q425 earnings reactions to MSFT, META, GOOG, AMZN already signal investor skepticism around exorbitant capex. An early defense against AI being framed as a bubble was that FCF, not debt, was funding the build out. That’s beginning to change with the emergence of ABS, SPVs, and off-balance-sheet vehicles. There’s no doubt LLMs are transformative. The internet transformed the economy too, but it did so after the dot com bust, and it took longer and benefited different companies than investors expected. Either ROI shows up soon or there will be blood.

The Orange Swan

The largest left tail risk is bright orange and very loud. You can’t miss him. Trump has ripped apart the federal infrastructure, filled critical leadership roles with unqualified cronies, and alienated our geopolitical allies leaving the US increasingly vulnerable to exogenous shocks. Executive overreach is likely to be the greatest shock of all. A domestic constitutional crisis is brewing and I expect federal interference in elections this November to make Jan 6th 2021 look quaint.

Tail Risk 1. Midterms

In early February, Trump said he wants Republicans to "nationalize the voting" and take over election administration in 15 states.

In a recent NYT interview, Trump said he regretted not ordering the military to seize voting machines after losing the 2020 election.

Trump has repeatedly threatened to invoke the Insurrection Act.

DOJ has demanded voter registration lists from states. 11 have complied, and more than 20 that refused have been sued.

DNI Tulsi Gabbard seized voting machines in Puerto Rico to examine them for foreign interference in the 2020 election.

The FBI raided a Fulton County election office and seized ballots from the 2020 election in late January. Gabbard was present at the scene.

Mass firings at CISA hobbled the federal infrastructure intended to protect against cyber threats to election integrity.

Recent executive order required proof of citizenship for voter registration, attempting to override states' constitutional authority over election administration (it was blocked).

Republicans in both the House and Senate introduced new SAVE Act proposals which would cause chaos in the midterms if passed by suppressing young voters and exposing election officials to significant legal risks.

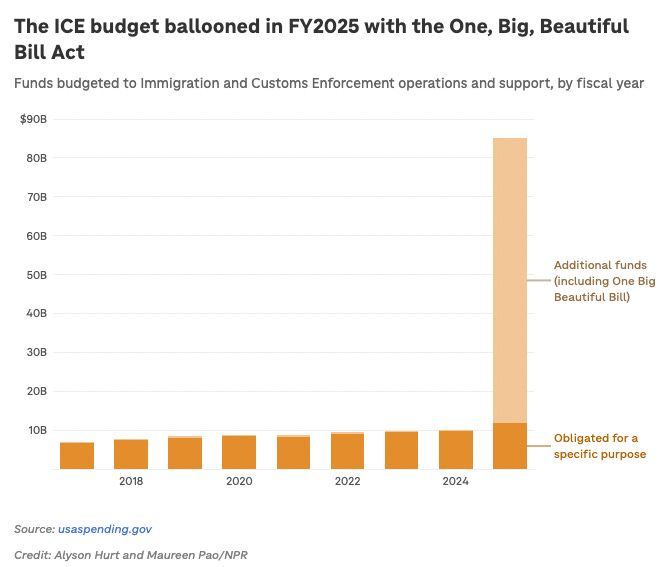

The pattern is clear. Elections are administered by states, not the federal government. The president has no authority to cancel or delay elections, but I expect to see ICE in key battlegrounds on election day. I view the operations in major liberal cities like Minneapolis as a beta test for federal authority, and thanks to the OBBBA, ICE’s budget just received a major ramp.

To be clear, depsite the interference, I expect Democrats to win the House by a wide margin. The tail risk is violent confrontations with masked agents at key polling stations, or claims of fraud used to justfiy a refusal to seat winning Democrats. If Trump tests the boundries of federal authority by invoking martial law and begins arresting political opponents it has potential for increased volatility and widespread civil unrest on a scale that impacts corporate earnings or awakens the bond vigilanties. I know this is a big what-if, but 15 years ago that scenario would have sounded like the ramblings of a lunatic; today, it’s plausible. We’re closer to autocracy in America than ever before. I remain optimistic about our future, but this risk is not fully discounted in 2026, and may become even greater in 2028 when (assuming he’s still coherent) Trump will undoubtedly refuse to leave office.

Tail Risk 2. Cybersecurity

The new cold war is online. Nearly half of all cyberattacks in 2025 were state sponsored and often masked as hacktivism or ransomware. In 2024, then FBI director Chistopher Wray warned Chinese hackers are preparing to "wreak havoc" on critical U.S. infrastructure including water treatment plants, the electrical grid, oil and natural gas pipelines, and transportation systems. He called this “the defining threat of our generation.” AI’s exponential improvement has only amplified this threat.

Instead of increasing cybersecurity defense budgets Trump hollowed out CISA, the main agency responsible for protecting American networks from foreign hackers, cutting 1/3 of its staff. Narly all of its senior leaders are gone. The Pentagon rolled back basic cybersecurity training for troops to prioritize “warfighting” while China and Russia are actively breaking into U.S. military and infrastructure systems. There’s also been talk of ramping up offensive hacking operations which risks enemies hitting back harder against the very defenses being torn down.

Tail Risk 3. The Next Pandemic

Another pandemic is inevitable, but the timeline is unknown. By withdrawing from WHO and killing USAID, the US has destroyed our early warning systems and international disease surveillance network. Trump signed an executive order halting all federal support for gain-of-function research which is pivotal for studying high risk pathogens. Massive funding cuts to drug and vaccine developments have kneecapped countermeasures in the research pipeline. OPPR, CDC, NIAID have all been gutted top to bottom. The US is facing outbreaks of diseases like measles and polio that were wiped out decades ago as vaccination rates are rapidly declining. Robert Kennedy Jr (possibly the dumbest human being to walk the earth) is somehow in charge of HHS. I don’t even want to imagine how another pandemic would play out today, but it would be much worse and even more politicized than covid.

Tail Risk 4. Seeds of The Next GFC

Deregulation is rolling back risk controls for financial institutions put in place after the 2008 crash. This will stimulate in the near-term but compound risk in the long-term. Those safeguards are the reason excessive leverage moved into the structural opacity of private credit. Private credit AUM has tripled since 2019 and many of these assets have investment grade ratings but wouldn’t hold a prayer under traditional scrutiny. SEC enforcement is at its lowest in a decade and the CFPB is effectively dead. Underwriting standards are not likely to improve in this environment.

Trump fired 19 Inspectors General who cumulatively saved taxpayers ~$71 billion in FY24 through fraud and waste investigations. There’s currently only six nominees for 28 vacant IG roles. We no longer have effective safeguards against financial mismanagement and fraud that could prove metastatic during a crisis. The ingredients of a toxic soup are simmering, but it’s likely years away from boiling over and not irreversible.

The Common Thread

Layers of protection have been compromised across elections, cyber defense, public health surveillance, financial regulatory oversight, national security coordination, disaster response, independent watchdogs, and the list goes on. No single cut is catastrophic in isolation, but weakened detection and response amplifes any tail-risk that comes to fruition. Eventually a crisis will occur, and the market’s lofty valuations, excessive leverage, and optimistic growth projections will be tested.

Long only investors, I wish you luck over the next few years.

Knife Catching 101

Short hand notes on some recent buys.

Bottom line: I am near-term bullish, medium-term bearish, and long-term always bullish on America. But price matters, and I’m finally seeing some decent prices for the first time since Liberation day.

SPGI - Post earnings, SPGI was -18% pre-market on what looked like a slight EPS miss. 18x forward for a business with unmatched pricing power and durability. I’m extremely skeptical AI will disrupt SPGI in any shape or form. The idea that AI will be capable of better ratings models is a red herring. First, AI needs access to reliable data, the ratings agencies are the most obvious source. Second, it’s never been about perfect models (hence the GFC), it’s about standardization. These are regulatory mandates for any business that wants to utilize credit markets. Either pay to get your debt rated by one of three agencies or costs go up. Simple as that. The only issue is Compounder bros bid this stock to the moon, so you can argue 18x is probably closer to fair than a screaming buy. I bought at $366 and plan to hold this long-term, but if we enter a bear market SPGI will go lower.

BAH – Small position. Civil segment still getting hosed but management signaled stabilization saying “the procurement environment feels like it’s at an inflection point.” The pipeline is growing, but funded backlog fell 10% and their EPS beat was driven by tax credits. TTM book-bill ratio down to 1.1x. In late January, Scott Bessent made a big show about cancelling $21M in Booz’s IRS contracts which quickly reversed the post-earnings gains. This is ~$5M annually which is a nothingburger. Mostly a theatrical punishment for a past Booz employee leaking billionaire tax returns. I expect Democrats to take the House and possibly the Senate later this year which should bode well for Booz’s Civil segment, but I want more confirmation that Civil has bottomed before I get too bullish. CEO recently bought $1M of stock.

FCN – ZIRP era debt is rolling into higher yields in tandem with Trump tariffs spiking input costs. If tariffs remain in place a wave of bankruptcies is coming. CEO recently bought $1M of stock, his first insider buy since 2017.

BRKR – Rapid margin expansion will provide robust earnings growth. Last year everyone expected a 30% cut to NIH’s budget, instead it grew 1%. Book-to-Bill ratio should continue to improve from pent up demand as delayed projects finally receive funding. Bruker would benefit greatly from a tariff pause. Trades a large discount to Life Science peers due to leverage, but CEO has a good track record of accretive acquisitions, owns a lot of stock, and deserves the benefit of the doubt.

AMZN - Unless you believe Anthropic is going to crash and burn over the next 12 months, Amazon looks good here. 24% growth in AWS (driven by increasing demand from Anthropic hence the large capex) and retail is booming with NA retail operating margins at 10%. No one can ever build another Amazon and it’s at historic low multiples despite strong growth and management finally running it with profitability in mind. If any business stands to benefit from AI efficiency and advancements in robotics, it’s Amazon. If and when the AI bubble bursts, AMZN will get punished as AWS estimates plummet.

PINS – Possible strategic target, steady growth, very cheap on adjusted earnings (I know, I know) and FCF given its growth profile. Activist pressure. PINS got hammered on weak guidance as it appears Meta is hurting them. I had a starter in the mid $19s and doubled the position in the mid $14s. I’m not sure why I bought this other than I thought it looked oversold into the print. I’m not sure why I added other than it seemed like an extreme reaction and is optically cheap. I don’t really know why Pintrest needs to exist at all and I’ll probably sell it sooner than later, bounce or no bounce.

FA – Outlined in my recent write up

UMG.AS – One of the most durable assets available in public markets. There will never be another record label at this scale. There will never be another catalog of music so deeply ingrained in the human psyche. I’ve been long around this price in the past and done well, but the market was more optimistic about streaming growth and UMG’s position in the value chain. It’s hard for me to call UMG cheap, but I think it’s a wonderful business at a fair price. I’m not a fan of Lucian Grainge’s exorbitant compensation. AI fear in this name is a joke. At $15 I’d make UMG a core position.

ADBE – Adobe is trading at 10x FCF. Terminal value was in question due to downmarket disruption from Canva and Figma before AI was on anyone’s mind. Now the market hates seat-based models and oh my god, did you see the incredible 15 seconds of Fast and the Furious slop someone made on Seedance?! People are lazy, and I’m glad. It’s growing double digits, and it’s not priced for decel it’s priced for death. The transition to a hybrid model is already taking shape with generative credits. AI is great at image generation, but not the last mile of editing. AI will be capable of generating multiple layers in the future, but I’m not sure LLMs will ever be capable of delivering a final edit. Adobe’s ecosystem moat is underrated. Every creative project in the last 30 years was built in one of their file formats, large enterprises are not going to abandon Creative Cloud. Generating slop on Midjourney that was trained on unlicensed IP might be good enough for a Mom and Pop’s social media, but large enterprises aren’t going to risk liability. Even Gemini offers no protection. Chances are Mom and Pop were already using Canva anyway. Adobe will continue to provide the gold standard in creative tools and generative AI is another tool. Distribution wins.

CSU.TO – Great culture, great track record, target pipeline has likely improved given the recent selloff. 16x Fw EPS. I prefer CSU to a software index like IGV, but this is more of a bet that AI will not displace VMS anytime soon.

NOW / IGV calls – Speculative bets that software is oversold. Big insider buy at NOW, trading at low multiples across the board with impressive growth and a very sticky platform. I probably should’ve bought shitco calls instead of IGV if I want to gamble.

A few others that have gotten interesting but not cheap enough yet:

7974.T (Nintendo) - memory shortage could be a big headwind.

TTWO - I’m long, but would add at $175.

CMG - I want this in the mid $20s, reaching midlife but I expect it will be durable.

COF - 1x Book or lower and I’ll get long.

SFM - I really like Sprouts, good managers, should be a steady grower and can take share from Whole Foods. Should thrive in the upper K based economy, but I want a lower price. Grocery margins still suck.

Disclosure

I am long ADBE, AMZN, BAH, BRKR, CSU.TO, FA, FCN, NOW, PINS, SPGI, TTWO, UMG.AS

This newsletter provides general ideas, not personalized investment counsel. All materials associated with this subscription and website, including articles, reports, and other features, are published for informational, educational and entertainment purposes exclusively. This content does not constitute investment advice, nor should it be interpreted as such. Any actions you take or decisions you make based on this content are entirely your own responsibility. Neither the author nor any affiliated parties will accept liability for any loss or damage, direct or consequential, arising from the use of the information provided.

This service does not issue trading signals, specific buy/sell recommendations, or any directive to trade. Nothing presented herein constitutes a solicitation or an offer to buy or sell any security. All sources are publicly available, but this information may contain errors. There is no guarantee, explicit or implied, that any ideas or securities discussed will replicate past performance.

The author may hold positions in the securities mentioned in these publications; these will be disclosed at the time of writing. There is no guarantee that the author will continue to hold these positions.

I agree with your assessment of the midterms and days/week after. IMHO, September to November won't be pretty, and maybe even into November. Even if "everybody knows", I think the fear will become unavoidable.